The trust upward has been very strong. Breadth on Thursday was 87% positive, the best so far in 2013 (chart). QQQ has been up 13 days in a row. We have seen this kind of streak before in 2013, in January, and know that it is bullish. Paststat has quantified the forward returns based on prior examples; more than 80% of the time, markets are higher 1-2 months out (post).

Add in a macro backdrop that has mostly been exceeding expectations recently (chart) and you have a pretty nice picture in the market right now.

The correction in May and June totaled 8% in SPX. You would think this would reset sentiment and prepare markets for the next leg higher into year-end. Recall that in every year except one since 1980, SPX has corrected at least 5% and in 80% of cases by 8% or more (post). In May, most pundits thought 2013 would be different but in the end the overwhelming probabilities for a mid-year correction won out yet again.

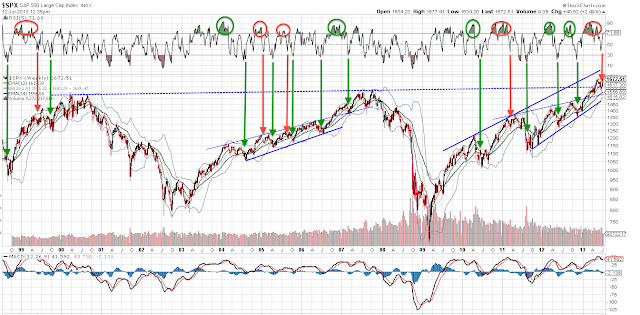

The rub, however, is this: the correction lasted barely a month. Moreover, the rebound has been a sharp V. That sharp a fall and rebound, in the past, has not immediately led to higher prices near term. Either the low has been retested or the market has consolidated over the next several weeks. In the first chart, this is shown by the prior V shaped corrections (green arrows). Notice that the better near term returns occurred when the correction and rebound were longer (the width of the red shading is 3 months).

This is also seen in weekly RSI; in the next chart, after becoming 'overbought' (circles), the successful rebounds have started from being very 'oversold' (green arrows); the shallow corrections (red arrows) eventually failed.

The reason behind these chart patterns is sentiment; a slower correction and rebound resets sentiment, bringing out bears and forcing bulls to question the outlook for the market. That happened to a certain degree this time (chart and chart) but not enough to get investors, both professional and retail, out of stocks and into cash, a set up that leads to the next successful leg higher. Wednesday's post detailed the current sentiment back drop more fully (read it here).

You can also see this in prior cases where markets have started strongly in the first half of the year; the second half of the year is overwhelmingly (89%) positive but the bulk of the returns (90%) have come after September, not during the summer. The summer, in other words, helped set up the rally into year end (from Stock Traders Almanac).

Seasonality in July is typically strong (green arrow in next chart), and this year is following that pattern. There are still 2 weeks left in July, but the pattern is typically weak in August and September (red arrow). Should this occur again this year, it would set up a very bullish pattern for 4Q.

In summary, trend and breadth, the two most important indicators, are looking very strong and expectations for the rest of 2013 are mostly positive. Welcome weakness should it develop during the remainder of summer.

Add in a macro backdrop that has mostly been exceeding expectations recently (chart) and you have a pretty nice picture in the market right now.

The correction in May and June totaled 8% in SPX. You would think this would reset sentiment and prepare markets for the next leg higher into year-end. Recall that in every year except one since 1980, SPX has corrected at least 5% and in 80% of cases by 8% or more (post). In May, most pundits thought 2013 would be different but in the end the overwhelming probabilities for a mid-year correction won out yet again.

The rub, however, is this: the correction lasted barely a month. Moreover, the rebound has been a sharp V. That sharp a fall and rebound, in the past, has not immediately led to higher prices near term. Either the low has been retested or the market has consolidated over the next several weeks. In the first chart, this is shown by the prior V shaped corrections (green arrows). Notice that the better near term returns occurred when the correction and rebound were longer (the width of the red shading is 3 months).

This is also seen in weekly RSI; in the next chart, after becoming 'overbought' (circles), the successful rebounds have started from being very 'oversold' (green arrows); the shallow corrections (red arrows) eventually failed.

The reason behind these chart patterns is sentiment; a slower correction and rebound resets sentiment, bringing out bears and forcing bulls to question the outlook for the market. That happened to a certain degree this time (chart and chart) but not enough to get investors, both professional and retail, out of stocks and into cash, a set up that leads to the next successful leg higher. Wednesday's post detailed the current sentiment back drop more fully (read it here).

You can also see this in prior cases where markets have started strongly in the first half of the year; the second half of the year is overwhelmingly (89%) positive but the bulk of the returns (90%) have come after September, not during the summer. The summer, in other words, helped set up the rally into year end (from Stock Traders Almanac).

Seasonality in July is typically strong (green arrow in next chart), and this year is following that pattern. There are still 2 weeks left in July, but the pattern is typically weak in August and September (red arrow). Should this occur again this year, it would set up a very bullish pattern for 4Q.

In summary, trend and breadth, the two most important indicators, are looking very strong and expectations for the rest of 2013 are mostly positive. Welcome weakness should it develop during the remainder of summer.