Individual investors ('retail') are now more long equity (65%) than they have been since September 2007 (blue line, below). Their cash balance (18%) is 6 percentage points below average. Their holding of bonds (17%) is at a 4 year low. In short, retail investors are already in the market. Can they get even more long? Of course, but the point is we are not at the beginning of the cycle. Readers of this blog know that professionally managed funds are likewise positioned long equity, short bonds (here).

Moreover, investors are continuing to pile into equities. In July, fund flows into mutual funds and ETFs reached an all-time high, surpassing the highs from the tech bubble peak in February 2000 (data from Trim Tabs).

According to JPM, retail net equity purchases (i.e., equities minus bond flows) is spiking. Investors are at an extreme risk-seeking mode at the moment. Yes, the prior peak was 2000.

At the start of a cycle, investors typically invest in safe large capitalization stocks. As the cycle matures and investors become more confident and willing to seek risk, they typically shift to technology and small cap stocks. To wit, daily sentiment towards technology is above the May peak and the highest in more than 5 years.

Similarly, small caps have been so strong that they have closed above their weekly Bollinger two weeks in a row for the first time since September 2012 (before an 11% drop). Chart here.

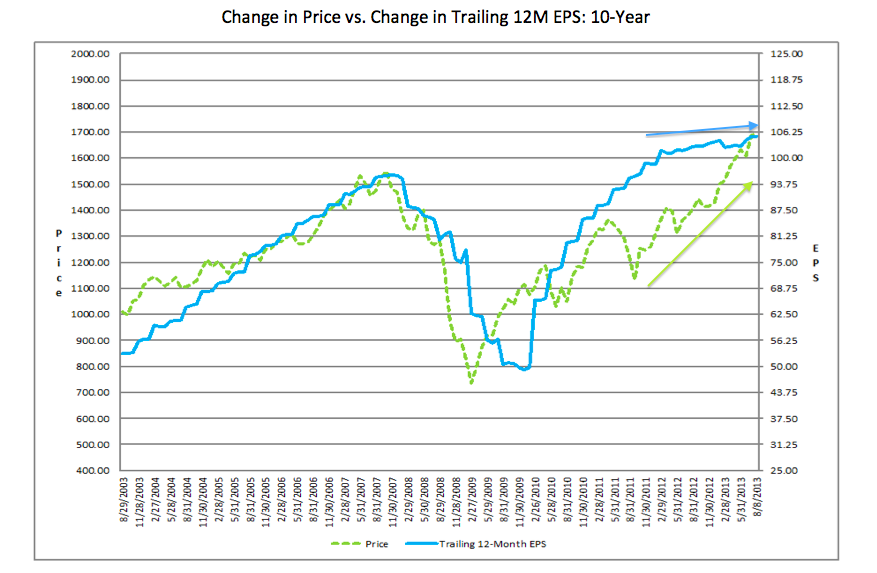

You don't need to look at esoteric research reports to see that investors have been getting long equities. In the past two years, the pace of increase in the SPX (green line, below) has far outstripped the growth in earnings (blue line), pushing price/earnings multiples well-above the 10 year average. This is the very definition of bullish investor behavior.

You can also look at the percentage of up days in the market to see how optimistic investors have become. In the year to date, more than 60% of trading sessions have been up. This has happened only two other times in the past 50 years: 1987 and 2007. These are notorious years where investors embraced risk to somewhat dire consequences.

The data, in short, do not support the assertions that this rally is hated or that investors are fearful and waiting to get into equities.

What does this imply for forward returns?

As we get deeper into 2013, investors should begin to think a bit about next year.

2013 will in all likelihood end with above average gains. This follows the above average gains last year. Since 1960, annual sequential gains above average (green arrows, below) have tended to be followed by below average gains in the third year (i.e., mean reversion; red arrows).

If you believe the US is at the start of a new secular bull market, this should be your base case for 2014. The only times in the past 50 years that the US indices have had more than 2 sequential above average years was at the end of the 16-year 1949-65 bull market and the end of the 18-year 1982-2000 bull market (yellow arrows, above and below). Prior to 1960, the exceptions were the demographically and fiscally exceptional pre- and post-war era.

Mean reversion is healthy and bullish for the market. It is the lack of mean reversion that has in the past been detrimental for future returns.