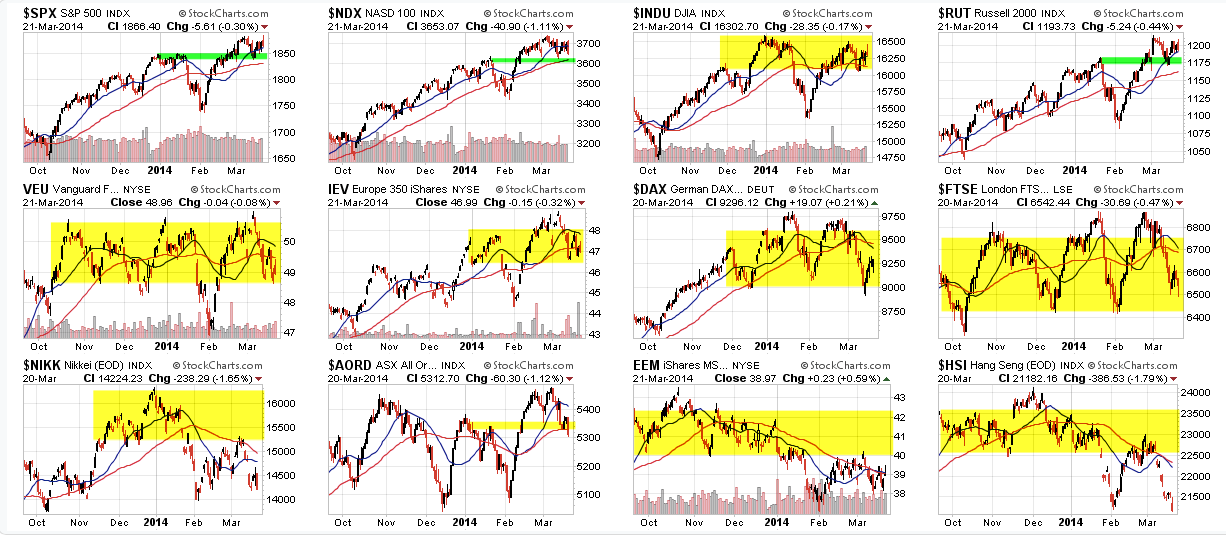

Equities made no progress in March. SPX was flat while RUT and NDX lost 3% or more. In comparison, treasuries, despite contrary comments by the Fed Chair, rose 1%. Given the torrid rise of equities in February, to say that March's lackluster performance was out of the consensus is a substantial understatement.

Entering 2014, analysts and pundits were expecting a repeat of 2013 (post). Things haven't turned out the way they expected.

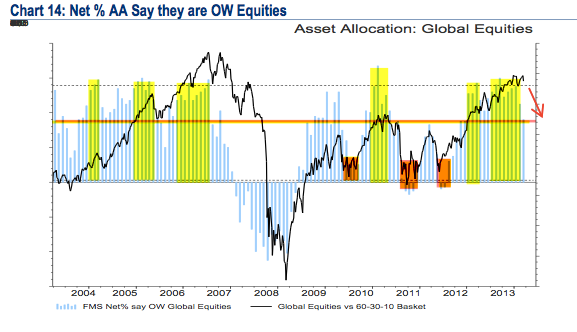

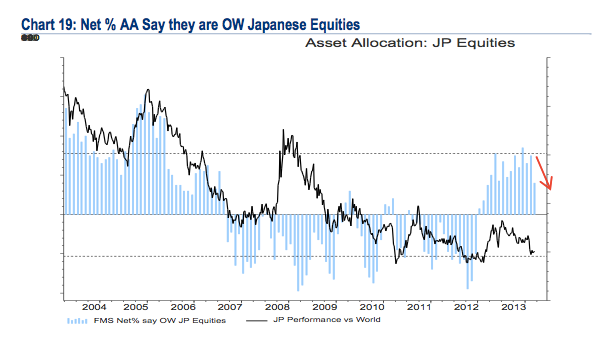

Investors have been massively underweight both commodities (far right, red) and fixed income (purple), both of which have massively outperformed; and they are overweight equities, especially technology (third bar) and small caps (fourth bar), which have declined.