In the event, SPX rose nearly 3%. In the process it exhibited a familiar pattern: overnight gaps in the past 4 days accounted 60% of the week's gain. Cash hours, when liquidity is greatest, was not where the meat of the gains took place. That was even more true for RUT and NDX which only posted cash hour gains during two of the four days.

After a sharp drop and a strong bounce, where does that leave the markets? Let's run through each of our market indicators.

Trend

Long-story short: trend is a mess. There is still a 1-year uptrend but there is also a 6-week downtrend.

Start with NDX. The positives are that it is still in a larger uptrend channel and its MACD and 13-ema are setting up for bullish cross on further strength. The negatives are that it was the only one of the US indices to trade below its February low, it hasn't made any net progress in four months, its under its 50-dma and there is a potential head and shoulders top being created.

RUT is not great either. The positives are that it held above its February low and the same MACD and 13-ema bullish cross may take place. The negatives are that it broke its larger uptrend channel and is now back-testing it; it's below its 50-dma; it hasn't made any net progress in six months; and it also has a potential head and shoulders pattern.

SPY is the most attractive of these three. Like NDX, SPY is still within it's larger uptrend channel (good). Like RUT, it has not breached its February low (good). But like both NDX and RUT, it has made lower lows and lower highs in the past several weeks (not good).

In the past two months, SPY has failed to break above 188 and below 183; in the chart below, note that it is in the middle of its volume by price range. Exceeding 187 would amount to a higher high (good) but there is more resistance just above at 188. Failure to exceed 187 would create another lower high (not good) and target the lower end of the range. In other words, what happens near 187 is key in the week ahead.

The sector level is equally messy. None broke their February lows (good). The cyclicals, except energy, all have a pattern of lower highs and lows over the past month (not good); utilities and staples (defensives) have the cleanest uptrends in place. That is generally not encouraging for equities which are driven by cyclical growth.

Ex-US markets are an equal mess. Europe is treading sideways with Australia, but Japan is making new lows. The upside leader is now the most hated market of all: EEM.

Bottomline: trend is not very encouraging. Markets are either digesting the big gains from 2013 or setting up for a larger fall in 2014. We have markers in place to give us a clarifying read in the week ahead.

Breadth

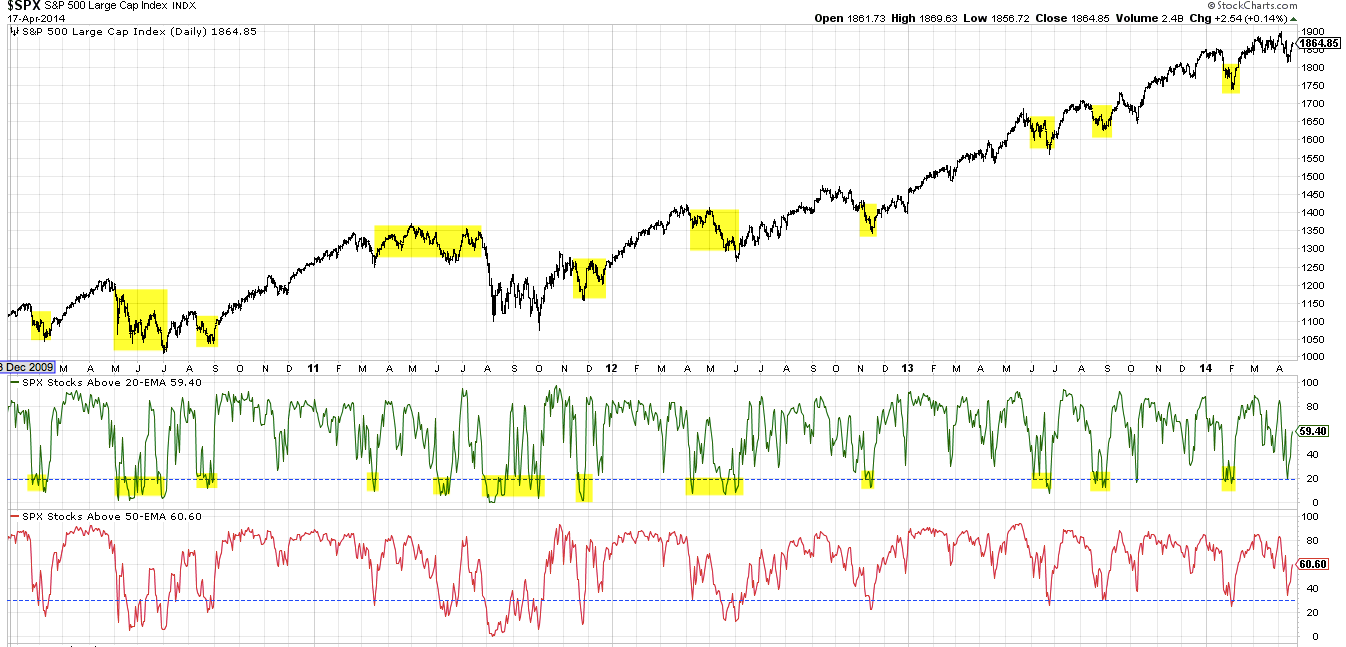

NDX and SPX both hit breadth extremes a week ago, a pattern for a short-term bounce. That started to play out this week and may have further to go. The dominant pattern, however, is for the indices to make a longer base at the low. In other words, those lows should be retested.

Start with SPX: since 2009, when only 20% of the SPX is trading above its 20-ema (middle panel), the index has exceeded those lows in the weeks ahead. The only v-bounce was in March 2011; this led to a 5-month sideways pattern and then a 20% drop. Net, at a minimum, the low should be retested if not exceeded in the weeks ahead.

NDX has the same pattern. There were no v-bounces off the breadth extreme in the past 10-years. The closest was in 2004 but that had an epic fail two months later.

Bottomline: breadth patterns suggest the current rally is sellable and a retest of the lows, if not a lower low, lies ahead.

Sentiment

The most bullish sentiment indicator is from AAII (retail investors). This week, the bulls fell to a level normally associated with a bounce in the indices (middle panel). The rub is this: investors didn't become more bearish. The bulls became neutral. In the past, at least 40% of retail investors are outright bearish at durable lows (bottom panel). This hasn't happened yet.

Overall, retail investors are long equities. Household ownership of equities is now back at levels from the 2007 top. The only time ownership has been higher was in the latter half of the 1990s (chart from GS).

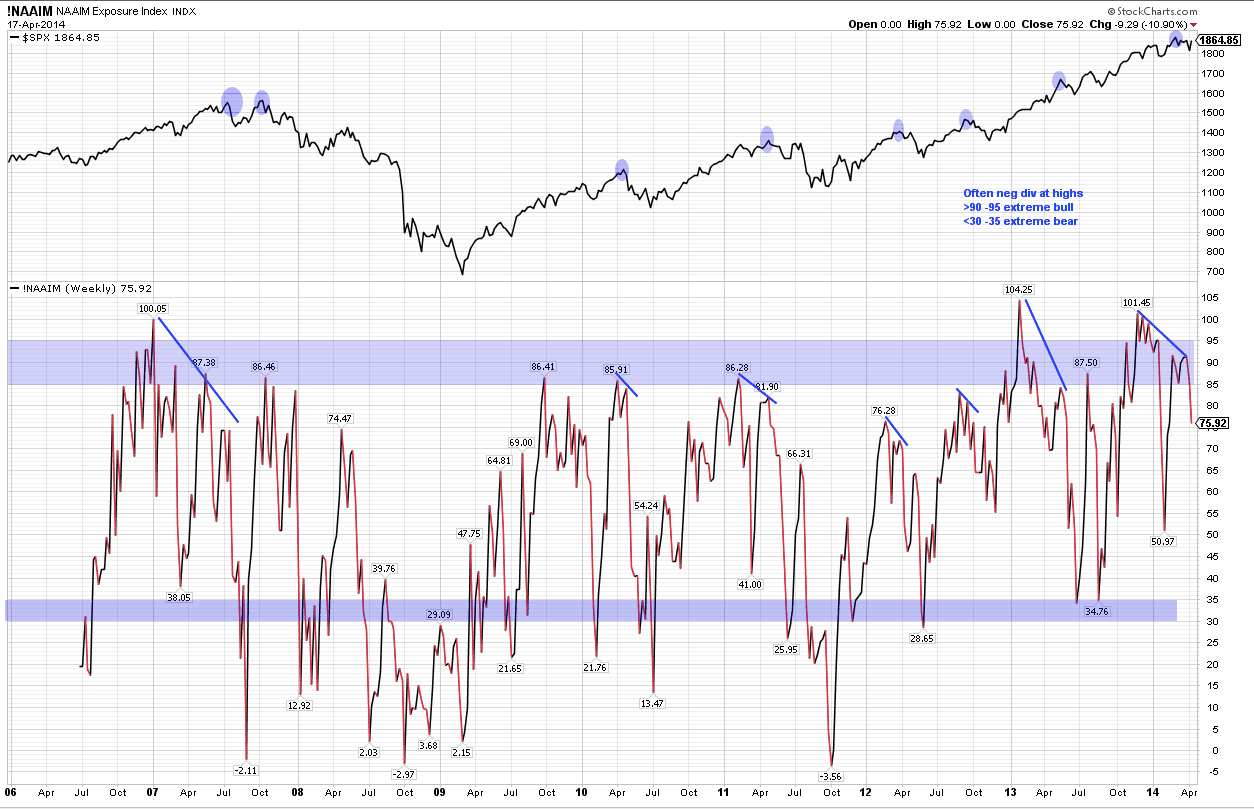

None of the other indicators of investor sentiment are set up for durable low in the indices. To take just one example, NAAIM (active investors) are 76% net long whereas durable lows occur when their position is less than 35% long. But more telling, their long skew is now the highest in 2014: the most bearish investor is neutral while the most bullish is 167% long.

BAML looks at fund managers' asset allocation once per month. A full review of the April results are here. What is remarkable is that equity markets are strongly underperforming bonds, yet funds increased their allocations to equities and further cut their underweight positions in bonds.

Moreover, funds increased their allocations to high beta sectors that have been underperforming in 2014 and yet remain highly underweight the defensive sectors that are handily being the indices. Net, professional investors, like retail and active investors, are still positioned for further upside. This is not how durable lows are formed.

Further, two-thirds of fund managers expect short rates to increase (i.e., short term treasury prices to fall). This is the most bullish funds have been on short rates since May 2011 (arrow). In the next few months, 5 year yields dropped dramatically. When a large majority expect an outcome, the opposite typically is more likely.

Finally, Sentimentrader looks at the percentage of IPOs that are from loss-making companies. When investors are demanding risky investments like these they are clearly not afraid of downside. This indicator is now back to levels present at the 2000 top.

Bottomline: sentiment is not a precise timing indicator in the short term, but the overall picture is one inconsistent with a durable low. This is especially important now after the excessive bullish positioning that has been taken up over the past year.

Volatility

Bottomline: Vix remains low. This is a pattern that was present for many years in the mid-1990s and the mid-2000s, both consistent with further market gains. In both periods, pull backs were limited to less than 10%.

Macro

While the meme in the market has been the current macro weakness is 'weather' driven, the bigger picture is that growth is positive but tepid. This is, in fact, the dominant pattern for any economy after a major financial crisis like the one recently experienced in the US.

We have been giving examples of positive but tepid macro growth every week in this summary. This week, real retail sales showed the same pattern: year over year growth of 2.2%.

Were growth accelerating faster, the bond market would likely be signaling expectations for greater future inflation. It isn't.

And the actual data on inflation this week continued the dominant pattern of weak pressure on prices (chart from Doug Short).

Growth outside the US is nearly as important, as roughly 40% of SPX profits are ex-US. The largest market is Europe. There is little to no growth in the Eurozone and inflation is falling.

When growth is weak and macro data is falling relative to expectations, equities tend to underperform bonds, and that is the pattern at present.

Bottomline: growth is positive but it's slow. In a fully valued market, the rate of growth sets the pace for equity appreciation. At present, the trend is for growth in the range of 2-4% for the year. That should be the limiting factor for equities for the time being.

Valuation

US markets, on any number of metrics, are trading at the high end of the range (more here). Looking just at PEs, the only time valuations were higher was during the latter half of the 1990s. In the big picture, valuations are at the tail end of the bell-curve (chart from GS).

Can valuations become more stretched? Yes. Is this likely? No. That's the message from a bell-curve: moving further into the tail implies declining probabilities.

Moreover, gains in equities over the past two years have been driven primarily by a revaluation higher (light purple bars). In the past, the third year is paced by actual earnings growth (chart from DB).

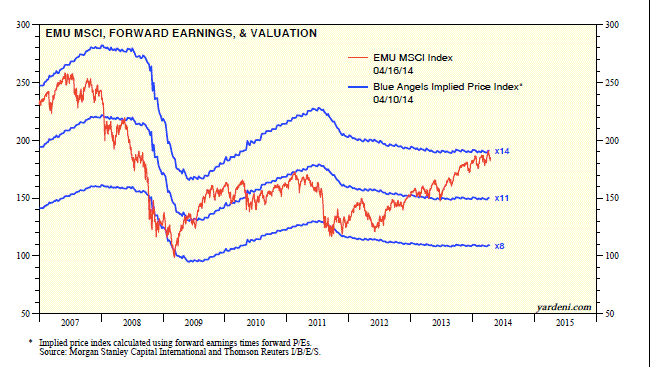

The situation is far more extreme in Europe. There has been no earnings growth yet indices have moved up to new highs in recent months. All of the appreciation since 2011 has been driven by a revaluation higher. Until earnings begin to grow, further appreciation is not likely (chart from Yardeni).

Is there valuation downside? Yes. Valuation multiples reflect future growth. When the yield curve is flattening, PEs normally move lower. Right now, the bond market is expecting slow growth yet equities are priced for high growth; someone is wrong (chart from Handelsbanken).

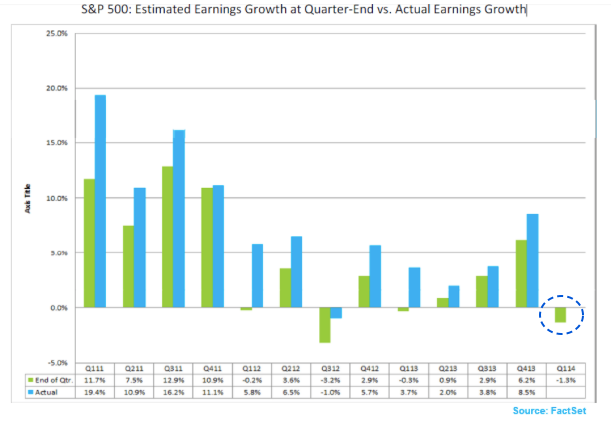

Right now, the bond market seems to the more right of the two. Per FactSet, 1Q14 EPS is expected to be negative. With 16% of companies reporting, the beat rate for both sales and earnings are below average. This is surprising given how low the bar has been set.

Bottomline: there's limited room for valuations to move higher, but if growth is weak there are precedents for valuations to move much lower. Our expectation for 2014 is for slow but positive growth in-line with the economy of 2-4%. We think this will limit appreciation to the upside.

Seasonality

The best six-month stretch for equities is from November to April. Gains during this period typically average 7.5%. Equities are now entering the weakest part of the year: gains from May through October average 0% (read more about this pattern here).

More importantly, lows tend to occur in the 'summer' months. As an example, look at the past 5 years: the lows occurred during the summer period (chart from Bianco).

.png)

2014 is also a mid-term election year. The typical pattern is for an early-year peak in the market and a low during the summer before a late-year rally. Here are the last four mid-term years, all of which exhibited this pattern (chart from Stock Charts).

In the short-term, the week ahead starts positive and then gets weaker. The following week is better: the last two days of April and the first few days of May are normally strong before further weakness sets in (chart from Sentimentrader).

Bottomline: equities have performed poorly year to date, and this is typically when they do best. Over the next several months, seasonality turns weak and this is when markets tend to find a bottom. A low in summer would likely set up a late-year rally.

* * *

Summary

Equities have been treading sideways in 2014, either digesting the gains from 2013 or forming a bearish top.

- Breadth suggests a retest of the lows from last week is still ahead.

- Seasonality suggests a more significant low is likely during the summer.

- Macro and valuation suggest upside will be limited by the rate of growth, currently 2-4%, but slower growth opens the possibility for a re-rating downwards.

- Volatility suggests that any weakness in the months ahead is likely to be limited to a less than 10% drawdown.

Most weeks recently have ended with a clear set up for the next week. That's not the case this week. We'll be watching SPY relative to 187 to determine whether a higher high or lower high will be formed. We'll also be watching the MACD and 13-ema in both NDX and RUT for direction.

Regardless of the short-term, the balance of evidence suggests that risk-reward is skewed to the downside over the next several months until the market experiences a washout.

Our weekly summary table follows: