Investors are used to higher US indices. In the past 27 months, SPX has had only 4 down months. That's an 85% win rate.

It's easy to believe, then, that this is unexceptional. Yet it is. It's not the streak itself that's so remarkable, it's the context in which it has been achieved.

Below is SPX since 1980, with every win streak of 5 months or greater marked. There have been 16 during this period.

The first point is this: context is the key to each win streak. In every case, the streak began after a drop in SPX. At a minimum, SPX traded down for 2 months in a row or traded sideways for the better part of a year before beginning its win streak. Every bear market low has been followed by a long win streak. The same is true for a 'correction' of 10% or more.

What's noteworthy, then, is that the context for the current win streak is very different.

Lost in the rear view look at the incredible 1990s is the fact that 1994 was a down year and 1992-93 gained just 4% and 7%. This was the set up for 1995 and 1996: what followed was two 8-month win streaks separated by just two down months.

Which brings us to today. SPX has been up 13% and 30% the past two years, nothing like the set up coming into 1995. Yet, since mid-2012, SPX has been up 7 months in a row, 4 months in a row and now 6 months in a row.

Second point: what is equally notable are the gains. During those win streaks in 1995-96, SPX gained 36% (after inflation). The current win streak from late 2012 is even better: 37%.

Yet the investment climate could not be more different. Real GDP was growing twice as fast in the mid-1990s as it has since 2011. Likewise, weekly employee earnings were also growing twice as quickly then as now, fueling consumption

The boom in consumption was evident in SPX earnings growth. Year over year growth in real earnings was more than 30% at the end of 1995. Today, the comparable figure is 7%.

In summary, the current run in the US indices is nothing like that of the 1990s. It is far more impressive. The gains have been larger, they have come with a profit and revenue growth a fraction of what they were in the 1990s and they have come, not on the back of a down year or two, but on the heels of a market that was already booming.

The third and final point is this: bull markets don't end with long monthly win streaks.

Refer again to the first chart above. Every gain since 1982 of at least 5 months in a row was always followed by a higher high. The worst outcome was a sideways market for several months. When the market fell, it was short and the gains were quickly reversed. For investors fearing a crash, that would be out of character with prior tops. More likely would first be oscillation between positive and negative months.

The Week Ahead

Our expectation was that US equities would struggle this week (post). In the event, SPX closed exactly flat, RUT and the Dow lost 0.7% but NDX gained 0.6%.

The big winner in the US was once again bonds. 30 year yields fell to their lowest level in 14 months. TLT gained 1% during the week. There's a negative RSI divergence on the daily chart for TLT. $114 is break-out support on weakness. Resistance above is light.

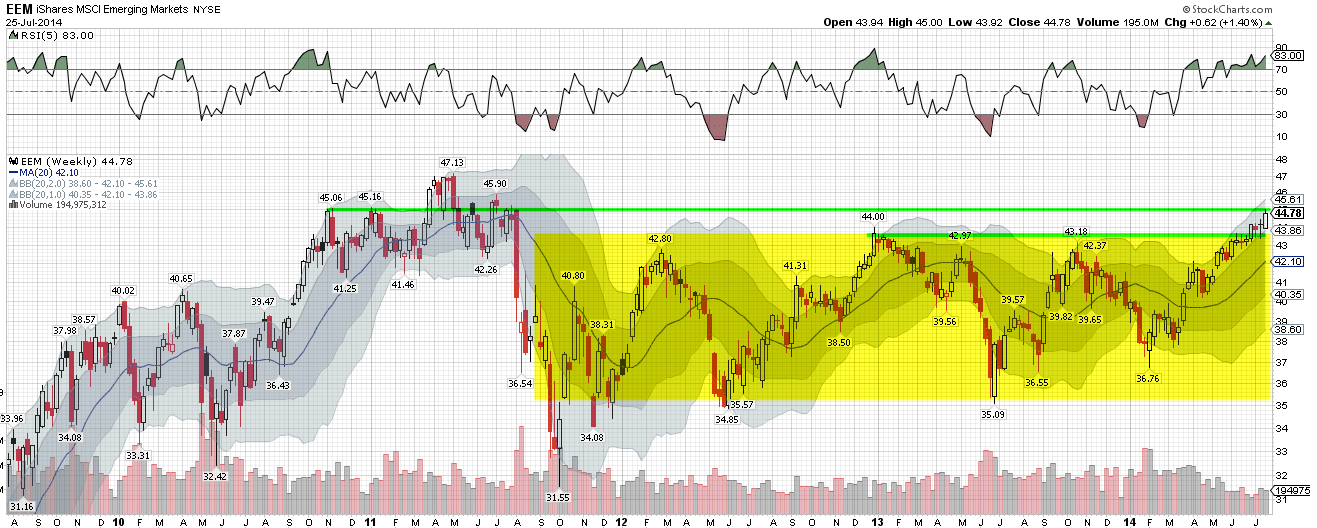

Within equities, the big winner continues to be EEM, gaining a further 1.4% this week. EEM broke out of its range from 2011 and is now back to $45, an important level from 2010-11 before price fell by 50%.

The gains in EEM are being driven by China, which gained more than 5% this week. FXI is now stretched to the upside and at a resistance level from early 2013. Some give back or consolidation would be normal.

As we have mentioned throughout 2014, both bonds and emerging markets have been universally disdained by investors, a lesson in the significance of crowded extremes.

For context, therefore, it is worth reiterating that investors in equities have reached an extreme in bullish sentiment (yellow shading) from which prices in the past have always retreated in the months ahead (for more on this, read here; chart from Short Side of Long).

Smart money seems to have taken notice. The open interest put/call ratio for the SPX indicates that these investors anticipate profit taking in the indices, or are at least hedging their positions. In the chart below, prior spikes in the past 10 years preceded a retreat; the last time was March 2012. The number of instances is low (chart from Paul Ciana).

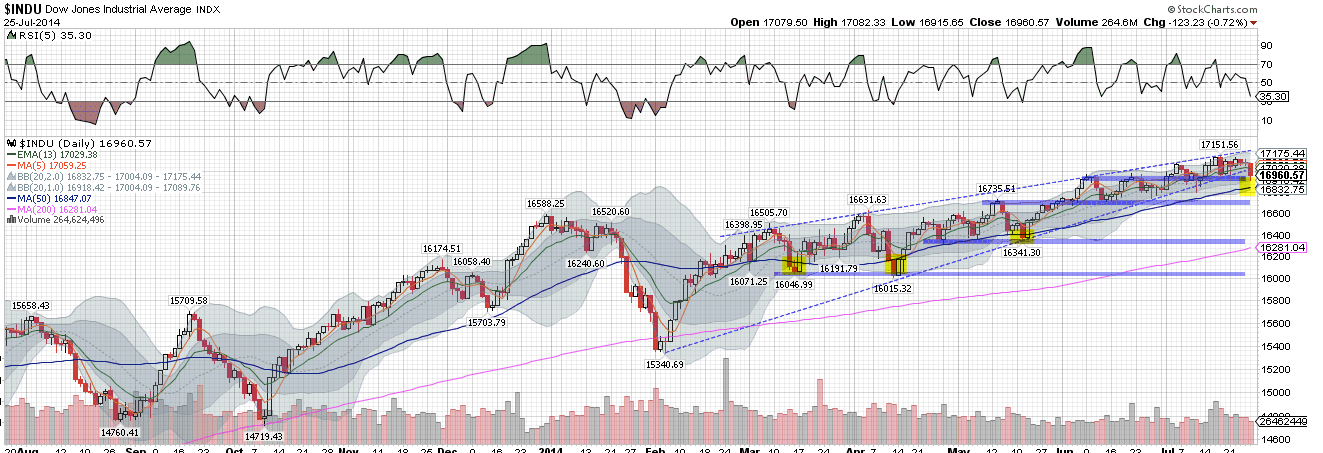

The Dow had a bad week. It broke a trend line from the February low and is below its 13-ema. All of its July gains are gone. But it is now on a support level with the 50-dma less than 1% lower, a key level to watch early next week. The 50-dma has held all sell offs from the February low (yellow).

RUT is the most bearish US index. It failed on the backtest of its 50-dma and prior resistance (1160 area) this week. Until that level is regained, the trend is lower. To watch is whether the 200-dma holds; it closed on it Friday. RUT has a negative return YTD in 2014.

NDX is easily the leader in the US. All of its moving averages are ascending. But it's upward progress is limited by the trend line from the June 2013 low (green line and arrows). It hit this trend line again Thursday. The 13-ema has contained every sell off since the April low.

SPY remains firmly in an uptrend. That said, it has made zero net progress since July 3. After clearing resistance at 198, it closed back below that level Friday. On weakness next week, 196 is the key; this is the trend line from the February low; weekly S1 is nearby at 196.4. On an overthrow, weekly S2 is 195 and it's also the July low. Watch the RSI for an emerging positive divergence.

From last week, it's worth reiterating that SPX is approaching 2000. In the past, there has been a strong reaction near each "round number" milestone; at a minimum, a decline of 3%, but usually more, occurs (chart).

Also worth reiterating is the loss of participation as the indices have moved higher. At the new highs this week, 40% of SPX companies were under their respective 20-ema. Nasdaq is worse: less than 50% are above their 50-dma. McClellan warned about the divergence in breath on Thursday:

The upcoming week will likely be macro-driven. 2Q GDP and the FOMC are both on Wednesday and employment (NFP) is Friday. Seasonality is a tailwind: July usually ends strong and NFP day has been up 17 of the last 20.

Our weekly summary table follows: