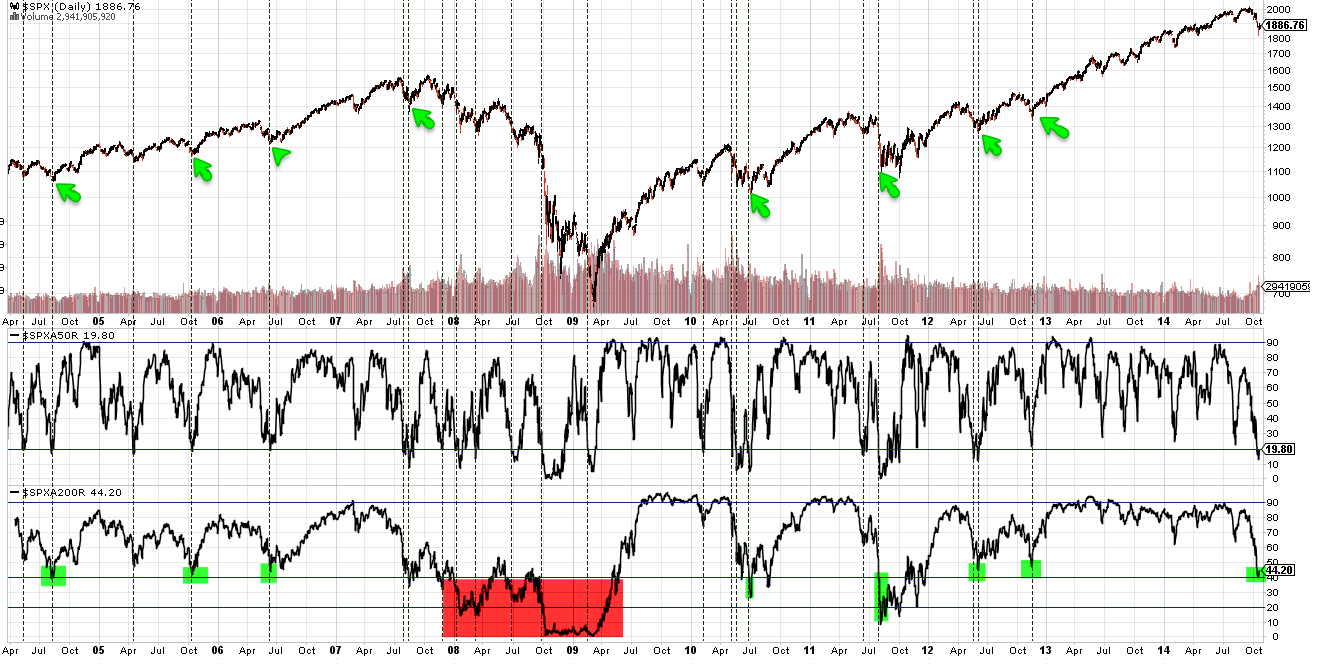

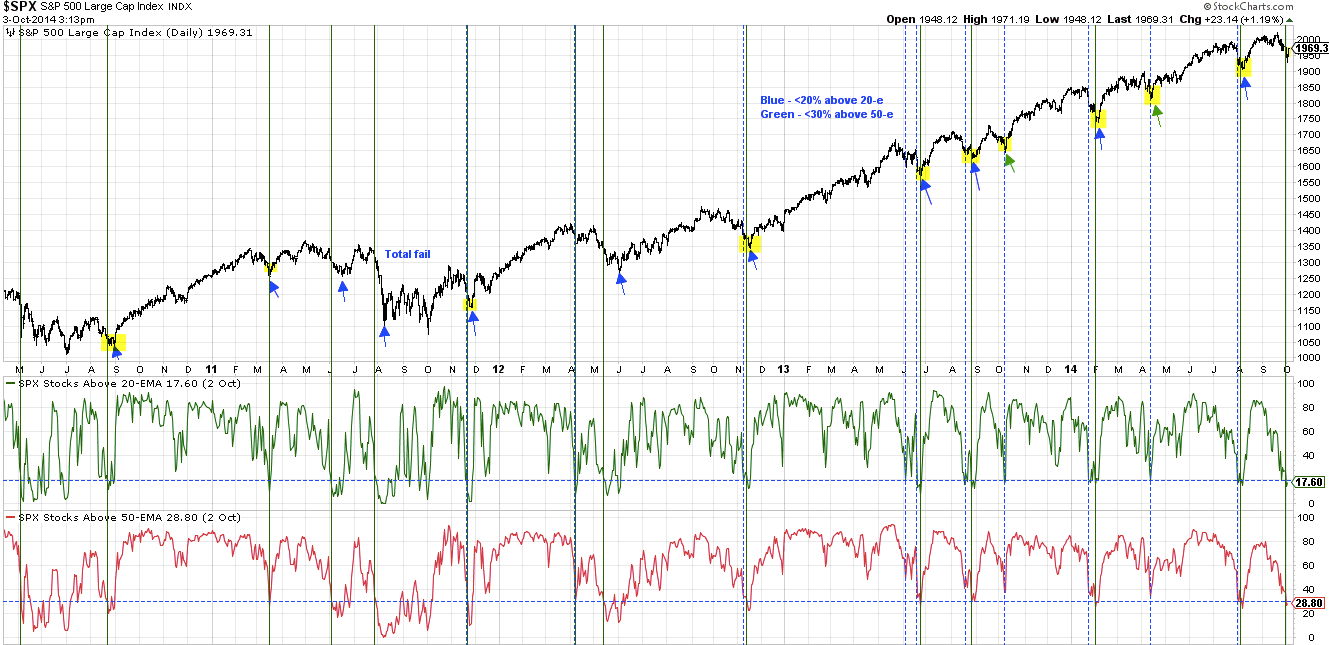

In May we started a recurring monthly review of all the main economic data (prior posts are

here). At the time, the consensus view was that growth in wages and employment were accelerating and that this would lead to a meaningful increase in inflation above the Fed's 2% target. So far, this has been wrong.

This post updates the story with the latest data from the past month. Highlights:

- The inflation rate continues to drop. It's well below the Fed's target of 2% yoy.

- Several measures of demand growth picked up: real retail sales growth was the highest in a year. Real GDP and PCE were revised higher to 2.6% yoy.

- New houses sold was the highest since May 2008.

Our key message has so far been that (a) growth is positive but modest, in the range of ~4% (nominal), and; (b) current growth is lower than in prior periods of economic expansion and a return to 1980s or 1990s style growth does not appear likely. This is germane to equity markets in that macro growth drives corporate revenue, profit expansion and valuation levels.

With the latest data, our overall message remains largely the same.

Employment is growing at less than 2%, inflation and wages are growing at less than 2% and most measures of demand are growing at roughly 2.5% (real). None of these has seen a meaningful and sustained acceleration in the past 2 years. The economy is continuing to slowly repair after a major-financial crisis.

This was the expected pattern and we expect it to continue.

We'll focus on four categories: labor market, inflation, end-demand and housing.

Employment and Wages

The September non-farm payroll (248,000 new employees) was slightly above the middle of a 10-year range. (The

past 12-month average of 220,000 was also in the middle of the range). This follows prints of 84,000 in December, 288,000 in June and 180,000 in August. Moving between extremes like these is nothing new: it has been a pattern during every bull market. Since 2004, NFP prints near 300,000 have been followed by ones near 100,000 (circles).