That's no longer the case. Fund managers became bullish again in December, and remain so now. Optimism towards the economy has surged to a 2-year high. Cash remains in favor (a positive) but global equity allocations are now back above neutral for the first time in a year. Another push higher and excessive bullish sentiment will become a headwind. The main exception to this is emerging markets, which are now out of favor and a contrarian long.

Findings in the bond market are of greatest interest. Fund managers' allocations to global bonds are now at prior capitulation lows. Moreover, inflation and growth expectations have jumped to the highest level since early 2011, after which US 10-year yields fell in half over the next several months.

The dollar is now considered the most overvalued in the past 10 years. Under similar conditions, the dollar has fallen in value in the month(s) ahead.

* * *

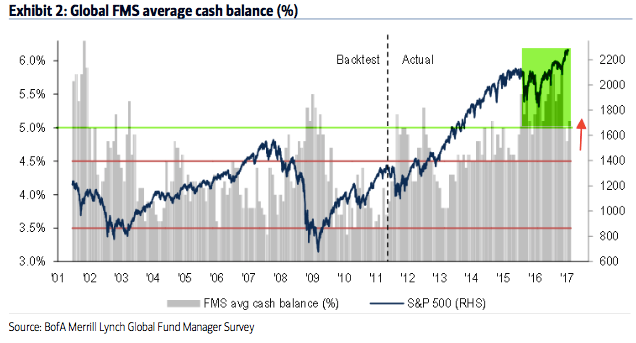

Among the various ways of measuring investor sentiment, the BAML survey of global fund managers is one of the better as the results reflect how managers are allocated in various asset classes. These managers oversee a combined $500b in assets.

The data should be viewed mostly from a contrarian perspective; that is, when equities fall in price, allocations to cash go higher and allocations to equities go lower as investors become bearish, setting up a buy signal. When prices rise, the opposite occurs, setting up a sell signal. We did a recap of this pattern in December 2014 (post).

Let's review the highlights from the past month.

Cash: Fund managers' cash levels dropped from 5.8% in October to 5.1% in January; cash is up slightly from December. Recall that 5.8% was the highest cash level since November 2001. Cash remained above 5% for almost all of 2016, the longest stretch of elevated cash in the survey's history. Some of the tailwind behind the rally is now gone but cash is still supportive of further gains in equities. A significant further drop in cash in the month ahead, however, would be bearish. Enlarge any image by clicking on it.