Fund managers have become more bullish, but not excessively so. Profit expectations are near a 7-year high and global economic growth expectations are near a 2-year high. However, cash balances at funds remains high, suggesting lingering doubts and fears.

Of note is that allocations to US equities dropped to their lowest level in 9 years in April: this is when US equities typically start to outperform. In contrast, weighting towards Europe and emerging markets have jumped to levels that strongly suggest these regions are likely to underperform.

Fund managers remain stubbornly underweight global bonds due to heightened growth and inflation expectations. Current allocations have often marked a point of capitulation where yields reverse lower and bonds outperform equities.

For the fifth month in a row, the dollar is considered the most overvalued in the past 11 years. Under similar conditions, the dollar has fallen in value in the month(s) ahead.

* * *

Among the various ways of measuring investor sentiment, the BAML survey of global fund managers is one of the better as the results reflect how managers are allocated in various asset classes. These managers oversee a combined $600b in assets.

The data should be viewed mostly from a contrarian perspective; that is, when equities fall in price, allocations to cash go higher and allocations to equities go lower as investors become bearish, setting up a buy signal. When prices rise, the opposite occurs, setting up a sell signal. We did a recap of this pattern in December 2014 (post).

Let's review the highlights from the past month.

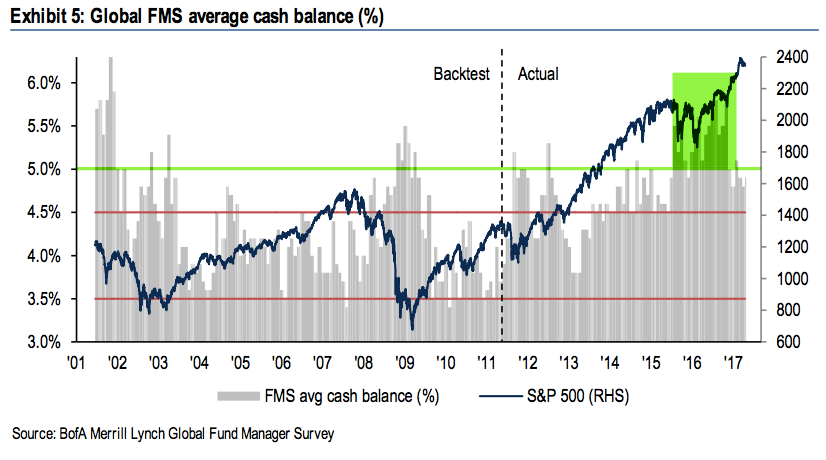

Cash: Fund managers' cash levels dropped from 5.8% in October 2016 to 4.9% in April. Recall that 5.8% was the highest cash level since November 2001. Cash remained above 5% for almost all of 2016, the longest stretch of elevated cash in the survey's history. Some of the tailwind behind the rally is now gone but cash is still supportive of further gains in equities. A significant further drop in cash in the month ahead, however, would be bearish. Enlarge any image by clicking on it.