* * *

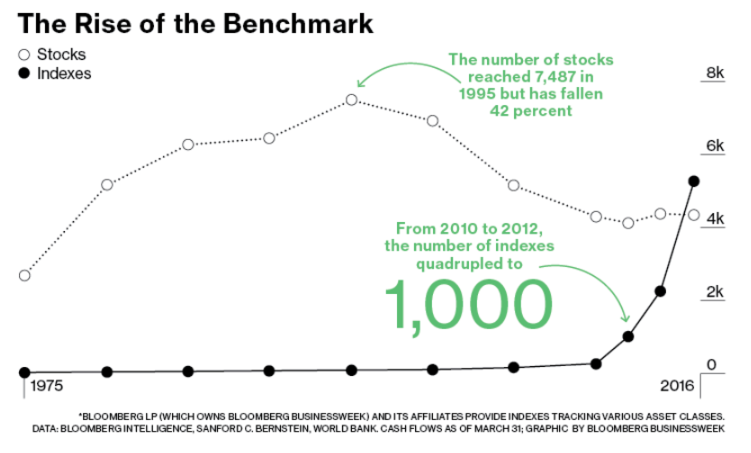

Bloomberg recently reported that the number of indexes has exploded and now exceeds the number of stocks in the US. Enlarge any chart by clicking on it.

This shift to index-based investing has been blamed for artificially compressing market volatility and for sowing the seeds of future stock market calamity. On balance, these claims seem hugely overblown.

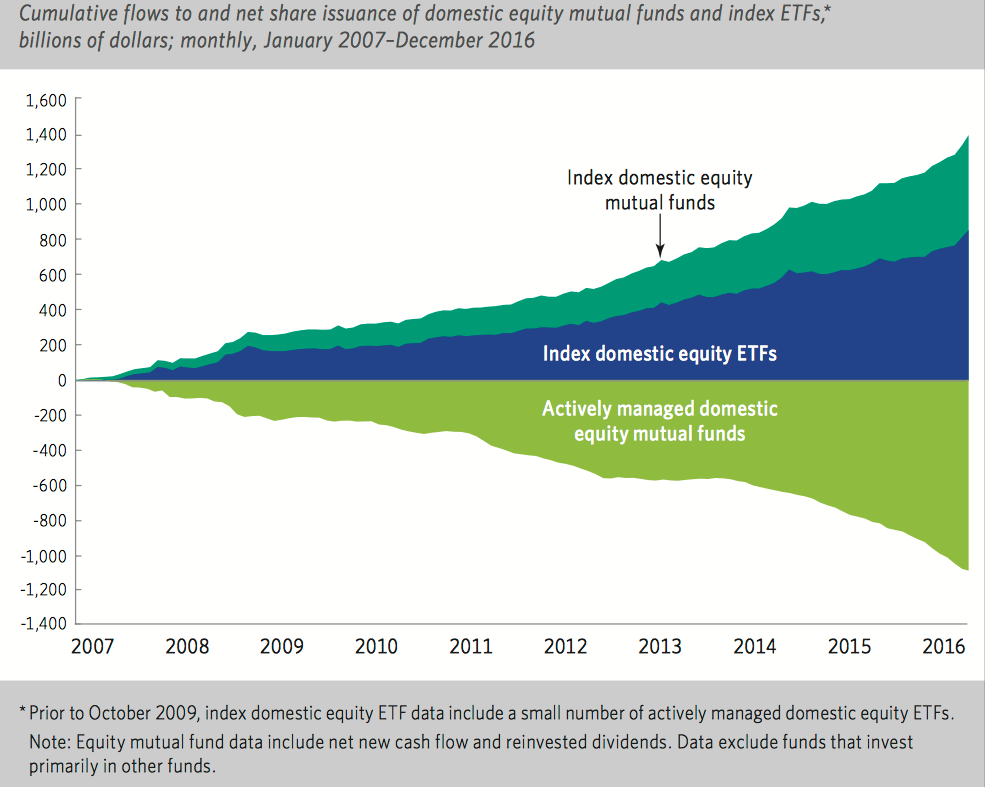

It's clearly true that there is a shift to index-based investing. Over the past 10 years, approximately $1.4 trillion has flowed into domestic equity index mutual funds and ETFs. About $1 trillion of this money has come out of actively managed mutual funds (from ICI; full report can be found here).

This has the look of a secular shift away from actively managed funds and into index funds: note in the chart above how fund flows did not reverse during the 2008 bear market. In other words, despite a devastating collapse in equity prices, investors added money to index funds and continued to pull money out of actively managed funds. The perceived value of active professional management, even during a tumultuous environment, was poor.

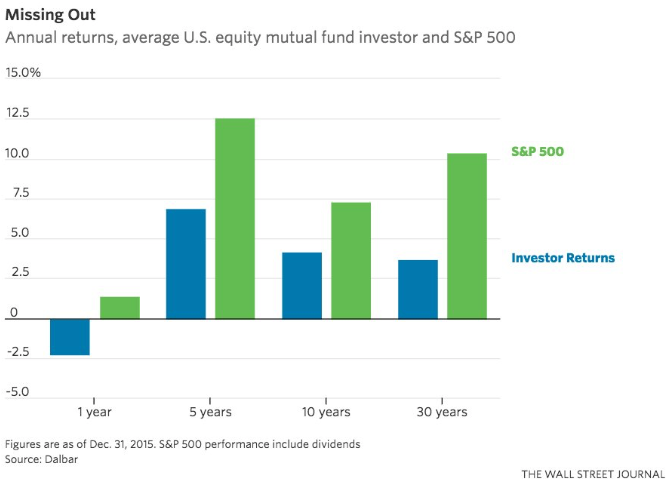

That is not so surprising, given the lower cost of index funds and their consistently better performance (green bars) relative to actively managed funds (blue bars; from the WSJ).

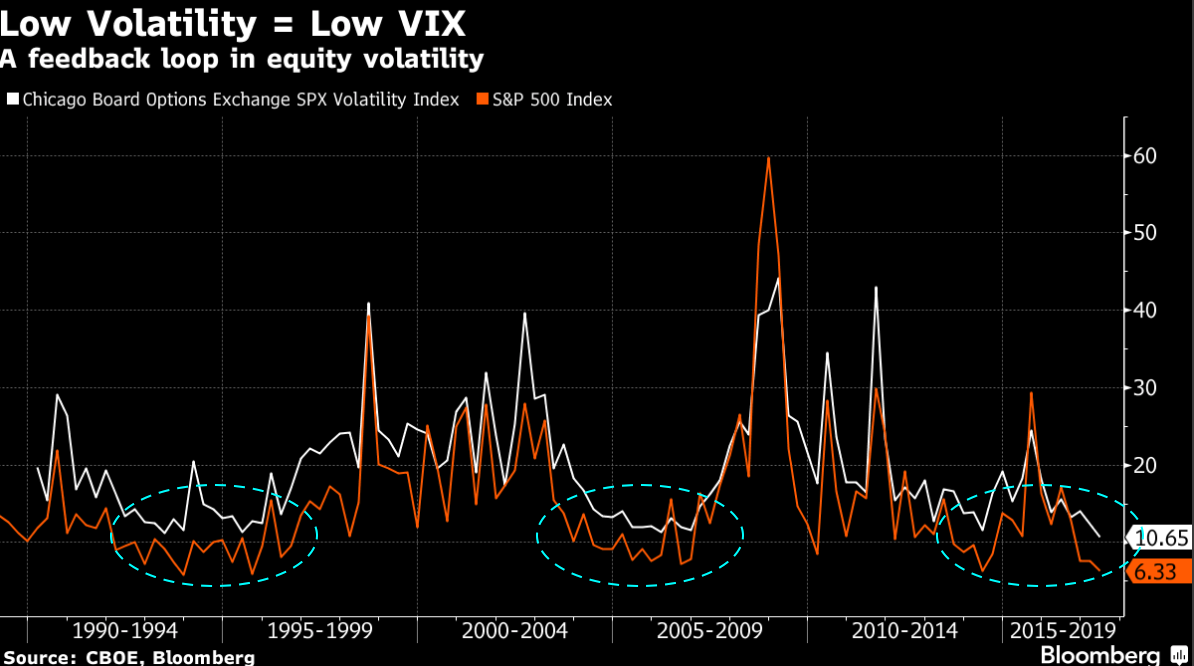

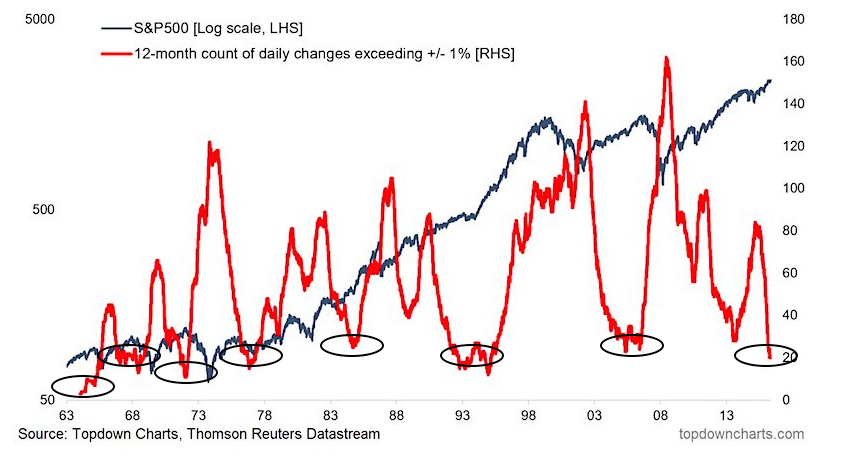

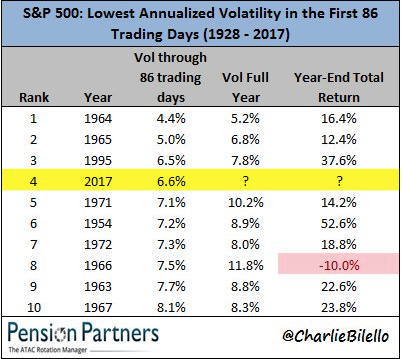

The shift towards index-based investing is being associated with the low volatility of the stock market. That seems unlikely. To begin with, a period of low volatility, measured any number of ways, has been a feature of every bull market for at least 50 years (from Bloomberg, Callum Thomas and Charlie Bilello, respectively).

More to the point, active management still accounts for the overwhelming majority of equity market ownership. The combined assets of all domestic equity index mutual funds ($2.1t) and ETFs ($1.5t) in 2016 equaled just 13% of the total US stock market's capitalization. Looked at a different way: in 2016, 31% of the shares outstanding in the US market were held in mutual funds and ETFs, of which about 1/3 was index-based. In other words, regardless of how it is calculated, nearly 90% of equity shares are "managed" not "indexed." It's hard to say that indexing itself is significant enough to compress market movements (data from ICI).

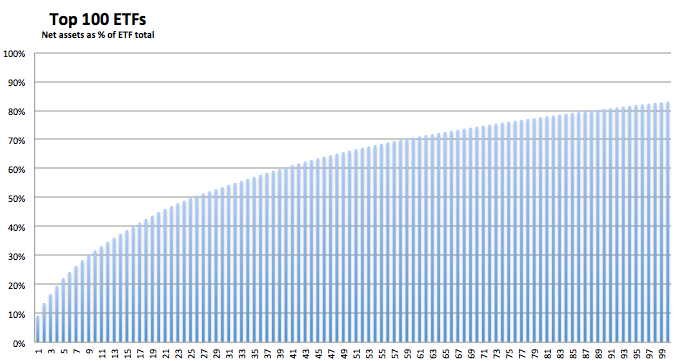

Moreover, while it's true that the number of index funds has exploded, the importance of this is massively overstated. For example, the number of ETFs has nearly doubled, to 2500, in the past 4 years, but:

The top 10 ETFs (0.4% of the total) account for a 1/3 of total ETF assets.

The top 50 ETFs (2% of the total) account for 2/3 of total ETF assets.

The top 100 ETFs (4% of the total) account for 84% of total ETF assets.

In other words, the concern over the proliferation of ETFs and index funds misses the key point that very little money is actually in the bottom 96% of them (data from ETF Data Base).

In summary, investors are clearly shifting away from actively managed funds to those based on index strategies. Only time will tell, but this has the look of a durable, secular change in investment management. But much of the perceived threat to market stability of indexing is overblown. Overall, the stock market is still dominated by active management. And while the number of index products has clearly exploded, 96% of these are of insignificant size.

In summary, investors are clearly shifting away from actively managed funds to those based on index strategies. Only time will tell, but this has the look of a durable, secular change in investment management. But much of the perceived threat to market stability of indexing is overblown. Overall, the stock market is still dominated by active management. And while the number of index products has clearly exploded, 96% of these are of insignificant size.

If you find this post to be valuable, consider visiting a few of our sponsors who have offers that might be relevant to you.