Summary: Global equities rose 22% in 2017. Throughout almost that entire period, fund managers held significant amounts of cash and were, at best, only modestly bullish on equities. All of this suggested lingering risk aversion following a recession scare in 2016.

As 2018 begins, cash levels have fallen to the lowest level in 4 years. Allocations to global equities have risen to the highest level in nearly 3 years. In most respects, investors are now bullish.

In the past 6 months, US equities have outperformed Europe by 12% and the rest the world by 2%. Despite this, fund managers remain underweight the US. US equities should outperform their global peers.

Fund managers are underweight global bonds by the greatest extent in 4 years. Only 4% of fund managers believe global rates will be lower next year, a level at which yields have often fallen, at least temporarily.

* * *

Among the various ways of measuring investor sentiment, the BAML survey of global fund managers is one of the better as the results reflect how managers are allocated in various asset classes. These managers oversee a combined $600b in assets.

The data should be viewed mostly from a contrarian perspective; that is, when equities fall in price, allocations to cash go higher and allocations to equities go lower as investors become bearish, setting up a buy signal. When prices rise, the opposite occurs, setting up a sell signal. We did a recap of this pattern in December 2014 (

post).

Let's review the highlights from the past month.

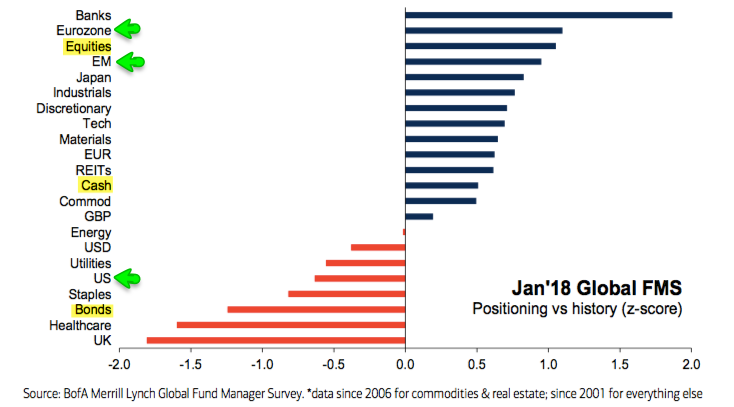

Overall: Relative to history, fund managers are overweight equities and underweight bonds. Cash is neutral. Enlarge any image by clicking on it.

Within equities, the US is significantly underweight while Europe, Japan and emerging markets are all significantly overweight.

A pure contrarian would overweight US equities relative to Europe, Japan and emerging markets, and overweight global bonds relative to a 60-30-10 basket.